The Beauty Pro Book Club: 4 Reads to Inspire Growth and Success

Four publications for beauty industry professionals to enhance their leadership skills, financial awareness, professional growth, and joy!

by Anne Moratto

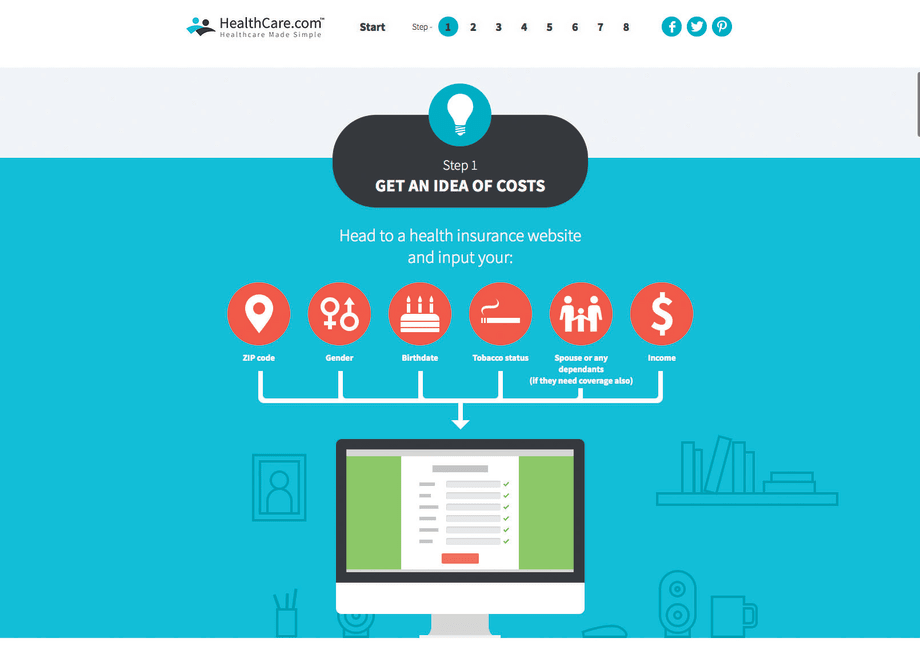

Think you can’t afford health insurance? Well think again. Since the Affordable Care Act became law, health insurance is easier to get and subsidies are available to lower the cost significantly. Follow these steps to find the right plan for you.

The average person’s definition of health insurance might read something like, “a nice-to-have luxury that is impossible to afford.” Health insurance was once a big-ticket expense. However, now that the Affordable Care Act (also known as Obamacare) is in place, all Americans have access to affordable medical coverage, many times for only $50 a month, depending on their annual income level.

One of the main reasons individuals remain uninsured is perception of cost. Many people don’t think they can afford health insurance, so they don’t even look at their options. But the reality is, the amount of money the government provides individuals and families to help pay for their monthly health insurance bills can cover more than 70% of the cost, if not more.

Moreover, having health insurance is required by law. In 2015, failing to buy a health plan can result in a fine of $325 per person or 2% of your income, whichever is higher. The fine is applied to your income taxes, so if you expect a refund every year but don’t have health insurance, you could wind up paying Uncle Sam a chunk of cash. The fine goes up to $695 per person in 2016, or 2.5% of your income.

The first step in buying health insurance is to think about it as a necessary product you would shop for at any given time. Take shoes, for example. When you shop online for a pair of shoes, you have many choices. What happens when you want to look for a certain color or a certain style? You filter your options to see only what you are interested in. Shopping for health insurance can work in the same way. Here are some of the basics you need to think about when filtering through healthcare plans:

Comparison shopping. Think back to the example of shopping for shoes online. Most individuals have 30-40 health insurance plans to choose from, so it’s important to line plans up and compare price, including extra out-of-pocket costs that come from deductibles, copays and coinsurance.

The color of the plan. Health insurance plans are categorized by “metal level,” which are bronze, silver, gold, or platinum. Bronze plans are the most affordable on a monthly basis, but you have to pay more money out of your wallet for medical care. Silver plans offer more insurance coverage, gold even more, and platinum plans typically cover up to 90% of medical expenses.

Medical needs. Think about how much you use healthcare in a given year. Do you see a doctor only once a year or do you have children who are routinely sick or have accidents playing sports? The amount of medical services you need in a given year should dictate how much insurance coverage you apply for. For example, if you see a doctor or visit urgent care 12 times in a given year between all of your family members, a health insurance plan with a lower deductible and copay options might be a better fit for your medical lifestyle.

Check the doctor and hospital network. Once you have narrowed your options to a few health insurance plans, check the provider network. If you want to see a particular doctor or urgent care clinic close to home, you should know in advance if the health plan you are most interested in will pay for services at the clinic you want to visit. This goes for hospitals as well. If you believe you will have at least one ER visit each year, make sure the hospital you visit is in the insurance company’s network.

See if you qualify for financial benefits to help pay for your plan. More than 87% of Americans who have health insurance through the federal marketplace qualified for financial benefits, also known as tax credits, on their health insurance in 2015. That’s an average cost savings of $263 per individual per month. If you haven’t checked on plan pricing, the handy tax credit calculator at www.healthcare.com/subsidy-calculator can help you estimate if you qualify for financial benefits on your health insurance.

The next health insurance open enrollment period begins November 1, or you can apply for an insurance plan before this date if you have a special event happen in your life, like getting married, getting divorced, having a baby, or moving to a new zip code.

You might think having health insurance is outside of your monthly budget, but it pays to look at all of your options, avoid paying a fine on your taxes, and ultimately, having coverage to help pay for the unexpected illnesses and accidents of life.

Colleen McGuire is vice president of communications for HealthCare.com, a leading health insurance search engine and comparison tool. The company provides a helpful interactive infographic here.

Four publications for beauty industry professionals to enhance their leadership skills, financial awareness, professional growth, and joy!

The most successful salon suites balance personality, function, and comfort. Megan Communale of My Salon Suite shares her best advice for designing a space that supports your business goals and leaves a lasting impression on every guest.

Square data shows that regular customers tip 11% higher and are shared across 32% of businesses in the same ZIP code, driving thousands of dollars in additional revenue per connection.

When Bowie Lau and Jeffrey Ching opened JBW Jeffrey Ching Salon in 2011, they weren’t just launching another luxury hair destination—they were building a business rooted in passion, artistry, and thoughtful growth.

Sponsored by Amex

Inside the Systems That Power an Elevated Salon Experience From seamless online booking to a team-first culture, J Gold Salon in Atlanta offers more than great hair—it delivers consistent, high-touch service with the help of partners like Boulevard and American Express.

Sponsored by Amex

Want to grow your career as a beauty professional? K18 Sales Manager Sabrina Sanborn shares advice on networking, mentorship, and self-advocacy—from attending hair shows to finding the right guidance to reach your goals.

A combination of clear policies, effective communication, and strong client relationships has helped me create a more reliable and efficient booking system.

Founded by Cleveland serial entrepreneur Shaura Rodgers, Nailtorious has grown to include a nail supply megastore, training facilities, and retail line for nail techs.

This period after the holidays can bring on a huge lull for hairstylists. We asked Cosmo Prof's team of professionals to offer their best advice on how to deal with the January-February slow period.

Key highlights include a push toward inclusive spaces for all abilities, an emphasis on maximizing livable square footage, and a continued love for modern farmhouse exteriors.

The busy holiday season is here, and with it comes jam-packed days, last-minute client requests and booming retail sales. For many salon owners, the highlight of the season is Small Business Saturday® (SBS). This year on Saturday, November 30, consumers can take their shopping into the small businesses in their communities.

Sponsored by Amex

Want to become savvy about your personal finances, but don't quite know where to start? Anna Manukyan identifies six important concepts for building a strong financial foundation.

Salon owner Nuri Yurt had a dream of owning a salon on New York City’s Madison Avenue. "Through perseverance, hard work and stellar customer service, he and partner John Kaygisiz founded Toka Salon in 2007.

Sponsored by Amex

This guide is your one-stop shop for a plethora of technology tools, software and services created to keep your salon or spa thriving.

Anna Manukyan shares a breakdown of what different types of financial accounts should be used for.

Vagaro has consistently been at the forefront of salon software technology, helping businesses be more efficient, create more effective communication, and even improve company culture. Now, Connect by Vagaro, the platform’s two-way communication capability, and Vagaro’s new generative AI tools are giving owners new opportunities to grow and expand.

Sponsored by Vagaro

Young Nails' Greg, Habib, and Tracey discuss whether getting too close to clients can damage your business.